The 2026–27 Budget and You

Linda Dang with a Client discussing changes in 2026 Budget

What every Australian worker, investor and aspiring homeowner needs to know

Published May 2026 · Budget Explained Series: Individuals

This article is general information only. Always speak with qualified accountants or financial advisers before making financial decisions.

The big picture

Last night's federal budget is being described by Treasurer Jim Chalmers as the most ambitious in decades — and for ordinary Australians, that's not just spin. If you earn a wage, own an investment property, are thinking about buying your first home, or are simply worried about the cost of living, this budget touches you directly.

Here's what actually matters, explained without jargon.

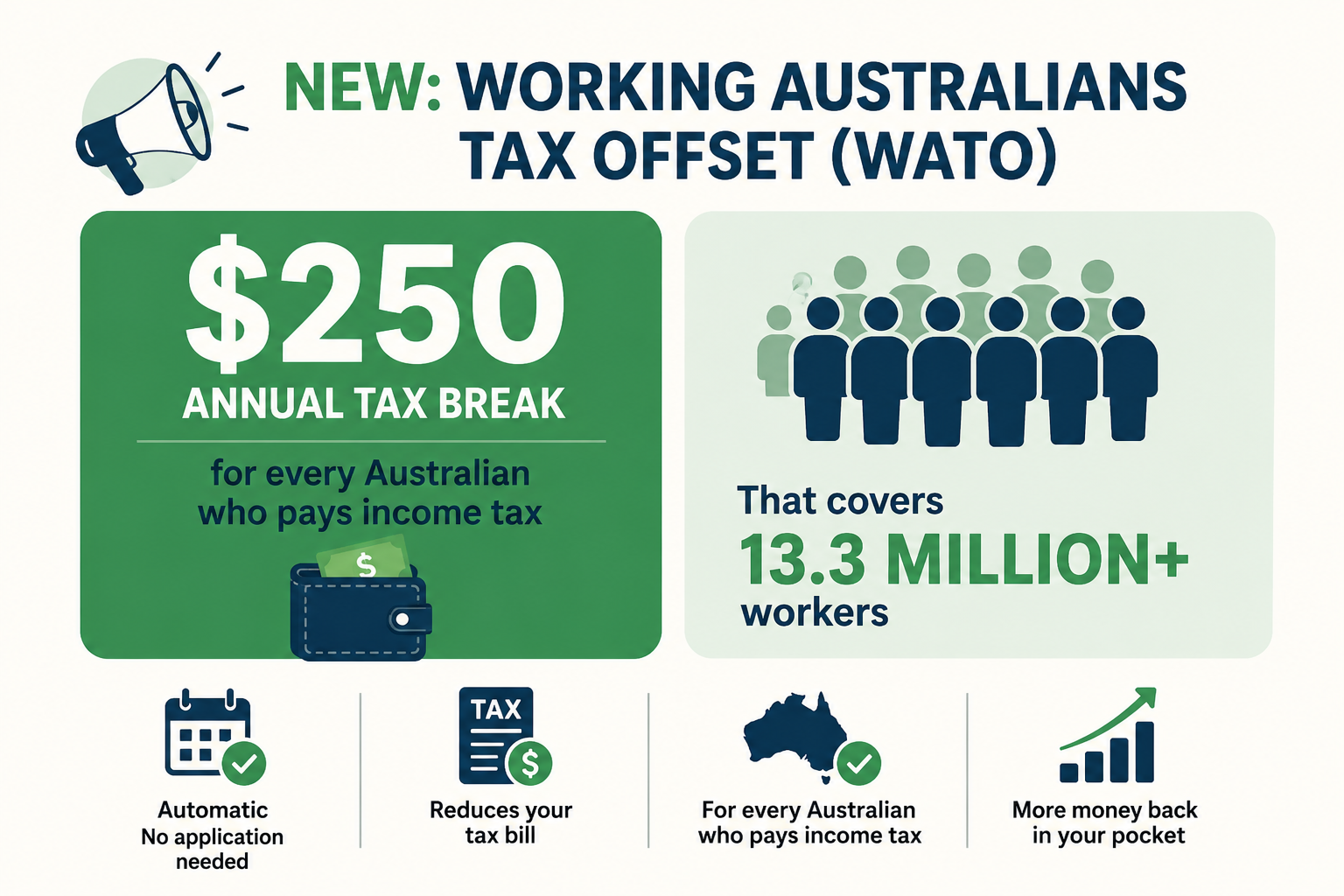

1. You're getting $250 back — but not yet

How the Working Australians Offset (WATO) works

What's changing

The government has announced a new Working Australians Tax Offset (WATO): a $250 annual tax break for every Australian who pays income tax. That covers more than 13.3 million workers.

When does it start

July 2028. This will not appear in your next tax return. It's a long-game cost-of-living measure that the government has committed $6.4 billion to over the first two years.

Who benefits

PAYG workers — anyone whose employer withholds tax from their salary or wages before it hits their bank account. If you lodge a tax return each year, this offset will come back to you annually once it begins.

The government's stated goal is to 'rebalance' the tax system — returning bracket creep to workers while increasing the tax contribution from passive investment income.

What you should do

Nothing right now — it's automatic. But understand that this offset is partly being funded by higher taxes on investment properties and trusts, which we cover below.

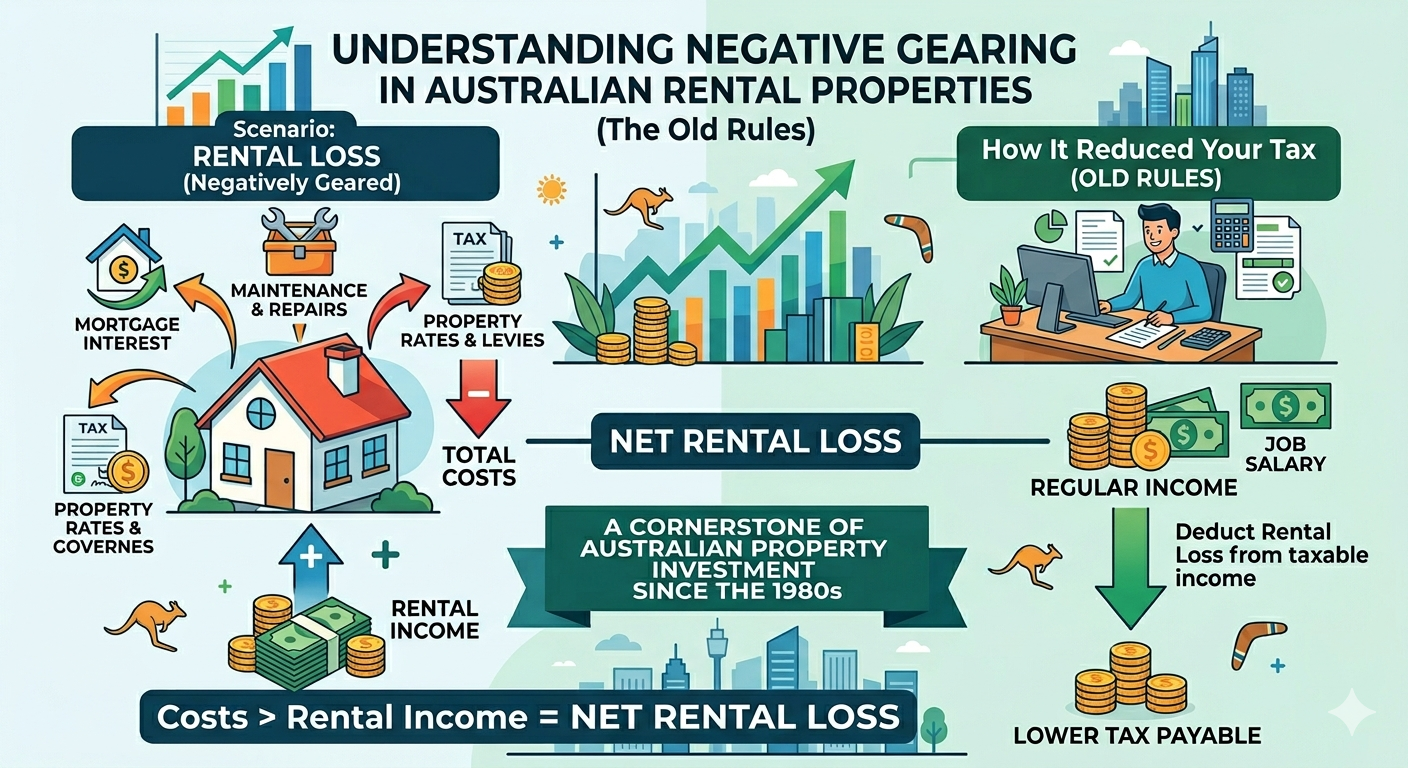

2. Negative gearing: the rules changed last night

Understanding Negative Gearing in Australian Rental Properties (The Old Rules)

What is negative gearing

If you own a rental property and your costs — mortgage interest, maintenance, rates — exceed your rental income, you're 'negatively geared.' Under the old rules, you could deduct that loss from your regular income tax, reducing how much tax you owe each year. This has been a cornerstone of Australian property investment since the 1980s.

What changed

From 12 May 2026, if you buy a new investment property, you can no longer negatively gear it — unless it is a newly built home. The deduction for rental losses against other income is gone for all existing properties purchased from tonight onwards.

What didn't change

If you already own a negatively geared investment property, nothing changes for you. You're completely grandfathered. This applies only to new purchases made after budget night.

The government estimates this change will help 75,000 additional Australians buy their first home over the next decade, by reducing investor competition for existing housing stock.

What you should do

If you were considering buying an investment property, the financial case has changed materially. Get advice from your accountant before you commit. If you're a first home buyer, this is a meaningful shift in your favour — though the effect will be gradual, not immediate.

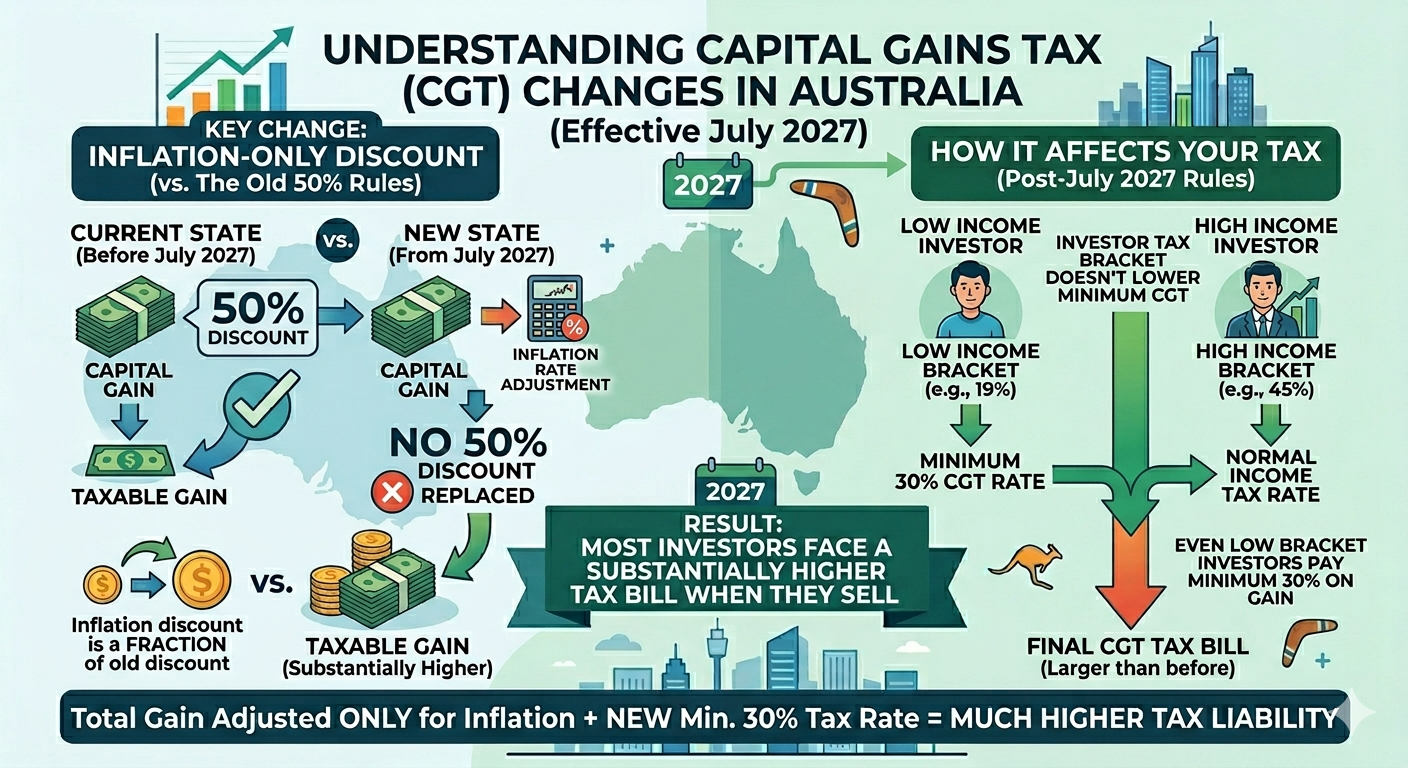

3. Capital gains tax: the 50% discount is ending

Understanding Capital Gains Tax (CGT) Changes in Australia

What is the CGT discount

Capital gains tax is paid when you sell an asset — shares, property, crypto — for more than you paid. Since 1999, if you held an asset for more than 12 months, you only paid tax on half the gain. The other half was completely tax-free. This 50% discount has made long-term investing significantly more tax-effective.

What's changing

From July 2027, the 50% discount is replaced by an inflation-only discount. You'll be able to reduce your gain by the rate of inflation over the period you held the asset — but nothing more. For most investors, that's a fraction of the current 50% discount and will result in a substantially higher tax bill when they sell.

On top of that, a new minimum 30% tax rate applies to capital gains. Even if you're in a low tax bracket, you can't pay less than 30% on a gain.

The exception

Investors in newly built homes can choose whichever discount — the old 50% model or the new inflation model — gives them the lower tax bill. This is the government's incentive to keep new construction attractive to private investors.

Transition period

Assets purchased before 30 June 2027 still operate under the old rules during a one-year transition. After that, the new settings apply universally to new purchases.

What you should do

If you've been sitting on investments you've been thinking about selling, talk to your accountant about whether the timing of that sale matters — it may matter a great deal. For ongoing investors, the arithmetic of holding assets long-term has changed.

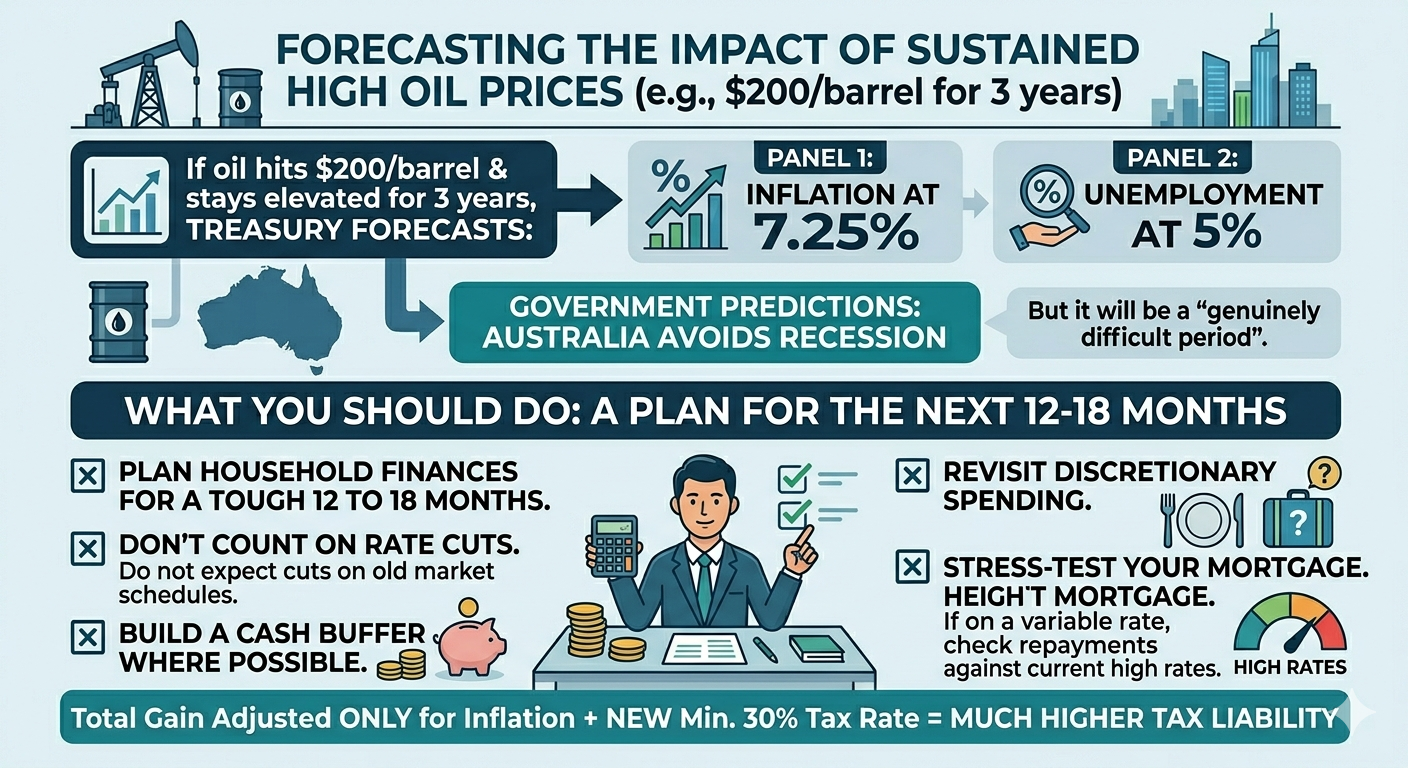

4. The inflation and interest rate reality check

What the budget says

The conflict in the Middle East — particularly the risk to oil supply through the Strait of Hormuz — is the dominant economic risk identified in this budget. Treasury's central forecast assumes oil stays at around $100 USD per barrel until the end of June, then falls gradually to $80 over the following year. Under this scenario, inflation peaks at 5% in the middle of 2026.

What that means in practice

Five percent inflation means your grocery bill, energy costs, and transport costs are rising noticeably. It also means the Reserve Bank of Australia is less likely to cut interest rates as quickly as many mortgage holders have been hoping. The RBA needs inflation back to 2–3% before it can ease rates — and at 5%, there's a real possibility that rates stay higher for longer.

The severe scenario

If oil hits $200/barrel and stays elevated for three years, Treasury forecasts inflation at 7.25% and unemployment at 5%. The government says Australia would still avoid recession, but it would be a genuinely difficult period.

What you should do:

Plan your household finances for a tough 12 to 18 months. Don't count on rate cuts coming on the schedule markets were pricing in at the start of the year. Build a cash buffer where you can. Revisit discretionary spending. And if you're on a variable rate mortgage, stress-test your repayments against rates staying where they are.

Forecasting the Impact of Sustained High Oil Prices

5. First home buyers: a real shift, but a slow one

What the budget is trying to do

The combined effect of the negative gearing and CGT changes is intended to reduce investor demand for existing properties — freeing up more of that housing stock for owner-occupiers and first home buyers. The logic is straightforward: if investment properties are less tax-advantaged, fewer investors will compete for the same homes first home buyers want.

The housing supply side

A $2 billion local infrastructure fund is aimed at unlocking 65,000 new home builds over the next decade by funding roads, sewerage and utilities in greenfield areas. This is complementary to the demand-side changes — the government is trying to both reduce investor competition for existing homes and increase the overall supply of new ones.

The risk

Treasury itself estimates that the investor tax changes could reduce new dwelling construction by around 35,000 over a decade, as property investors who fund apartment development pull back. The infrastructure fund is meant to more than offset this, but it's a genuine risk worth watching.

What you should do

If you're a first home buyer, the structural environment is improving — but this plays out over years, not months. Keep saving. Take advantage of every first home buyer grant and scheme currently available. Don't wait for a market correction that may not arrive in the near term.

The bottom line for individuals

This budget makes some genuinely significant long-term changes. The property tax system has been restructured in a way that hasn't happened in decades. Workers will eventually get a meaningful tax break. And the housing market is being tilted — slowly — in favour of owner-occupiers.

But the next 12 to 18 months will be financially challenging for many households. Inflation is elevated, rate relief is uncertain, and the cost of living is not going to ease overnight.

The best thing you can do right now is understand what's changed, take professional advice where it's relevant to your situation, and make sure your financial position is as resilient as possible for a period of genuine uncertainty.

This article is general information only and does not constitute financial, taxation or legal advice. Please speak with a qualified accountant or financial adviser before making decisions based on budget measures.

The 2026-27 Federal Budget represents a fundamental shift in how wealth and property are treated in Australia. While the headlines focus on long-term tax offsets, the immediate reality for investors and business owners involves navigating a much stricter landscape for capital gains and rental deductions. Success in this new environment won't happen by accident; it requires a proactive strategy that aligns these legislative changes with your unique financial goals. Before the next financial milestone arrives, let's ensure your portfolio is structured for resilience rather than risk.