The Payday Super Revolution: What Every Australian Business Needs to Know Before July 1, 2026

Australia’s payroll system is changing in 2026, with superannuation moving from quarterly payments to payday super.

For more than 30 years, the rhythm of Australian business has been driven by the "quarterly super run." It’s a date marked in every bookkeeper's calendar: the 28th day after the quarter ends. But on July 1, 2026, that rhythm is set to change forever.

The Australian Government’s "Payday Super" legislation is no longer just a proposal—it is now a law. This change is the biggest revolution in the payroll landscape since the introduction of Single Touch Payroll (STP). It’s a big win for the retirement savings for employees and for employers, it’s a fundamental shift in cash flow and compliance that requires preparation starting today.

What is Payday Super?

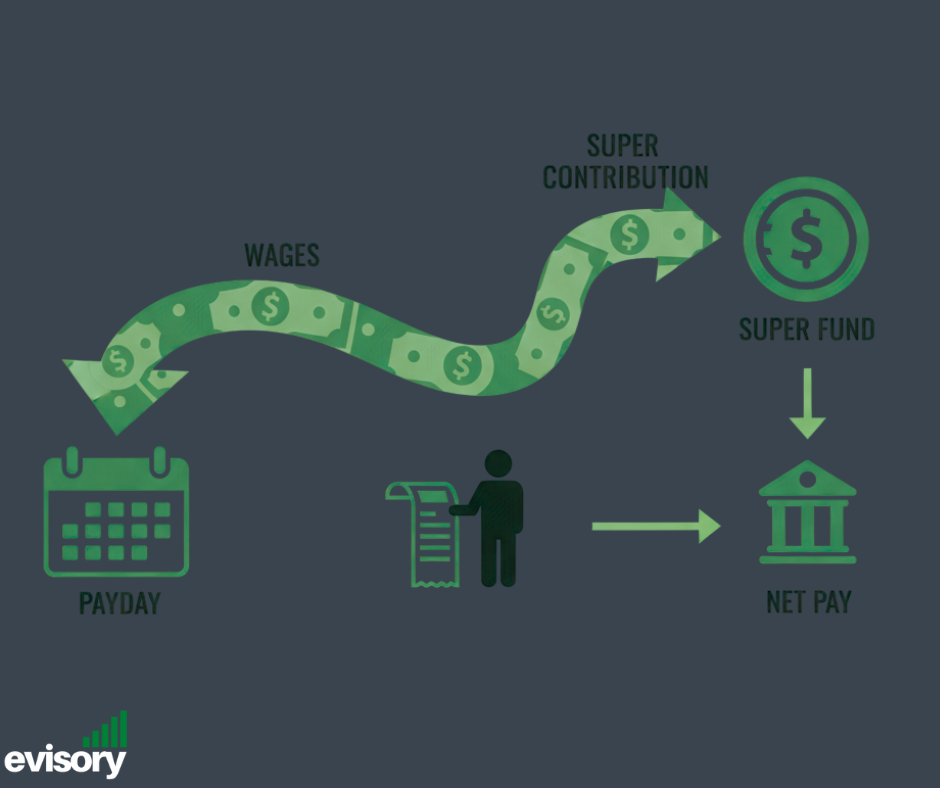

Under Payday Super, employers must pay superannuation at the same time as wages, rather than quarterly.

At present, most employers give Superannuation Guarantee (SG) contributions on a quarterly basis. However, under the new rules, employers are now required to pay their employees' super at the same time they pay their salaries and wages.

In short: If it’s payday for wages, it’s payday for super.

This new scheme requires that super contributions be made to the employee’s chosen fund within seven business days of payday. Although the rate of contribution will still be calculated at the legislated rate (which will be set at 12% by 2026), the frequency of payment will jump from four times a year to as many as 52 times a year for weekly payrolls.

Why the Change?

More frequent super payments help reduce unpaid super and improve long-term retirement outcomes for employees.

The ATO estimates that the "super gap"—the difference between what is owed and what actually gets paid—is approximately $3.6 to $5 billion per year. With the superannuation system now being tied to wages, the government seeks to:

Reduce Unpaid Super: With real-time tracking, it becomes much more difficult for payments to go unpaid, particularly in instances of business insolvency.

Boost Retirement Savings: Smaller, more frequent deposits benefit from "compounding interest" much earlier. Treasury modelling suggests that this alone is projected to see a 25-year-old, on a median wage, have an additional $6,000 in their retirement savings simply due to this change in timing.

Enhance Transparency: Employees will be able to track when their super payments are made to their accounts in near real-time, matching their payslips.

The Technical Shift: From OTE to "Qualifying Earnings"

From July 2026, super calculations will move from Ordinary Time Earnings to Qualifying Earnings to simplify payroll reporting.

One of the more technical nuances of the changes in July 2026 is the introduction of a new concept: Qualifying Earnings (QE).

Whereas at present, super is calculated on "Ordinary Time Earnings" (OTE), the new system will calculate on QE. This is designed to simplify what is included in the super calculation, effectively bringing together OTE and other payments (like salary sacrifice) into a single, clearer reporting category for Single Touch Payroll (STP).

Key Challenges for Small Business

Payday Super introduces new cash-flow and compliance challenges for Australian small businesses.

Although the advantages for employees are clear, the Institute of Public Accountants (IPA) and other industry associations have observed that the changeover will be “a shock” for small businesses. There are three main challenges:

1. The Cash Flow Crunch

For decades, businesses have relied on the “super money” in their bank accounts as a safety net for cash flow. Moving to payday super means that money leaves the business immediately. In July 2026, businesses will experience a “double hit": they must pay the final quarterly installment for the April-June 2026 period and start the new payday payments simultaneously.

2. The Retirement of the Clearing House

The ATO’s Small Business Superannuation Clearing House (SBSCH), which is now used by hundreds of thousands of small business employers, will be retired on July 1, 2026. Businesses currently relying on this free service will need to find a private alternative or use the clearing house integrated into their payroll software.

3. Stricter Penalties

The "grace period" of the past is being phased out. Under the new regime:

The 7-Day Rule: Contributions must be received by the fund within seven business days.

Compounding Interest: If you miss the deadline, the Superannuation Guarantee Charge (SGC) will be charged with daily compounding interest.

Administrative Uplift: A new "uplift" penalty (replacing the old $20 fee) could be as high as 60% of the shortfall.

How to Prepare: A 5-Step Checklist

Early preparation helps businesses transition smoothly to Payday Super before July 1, 2026.

July 2026 might seem far away, but because this change is so structural, the ATO and tax professionals recommend acting now.

Review Your Software: Talk to your payroll software company (Xero, MYOB, QuickBooks, etc.). Make sure they are updating their systems to handle "near real-time" payments through the New Payments Platform (NPP).

Audit Your Data: Incorrect employee details (TFNs or fund USIs) are the main reason for failed payments. With only a strict 7-day window, you won't have time to fix errors after the event. Use the new "Member Verification" functionality to check information before July 2026.

Transition Your Clearing House: If you are using the SBSCH, it’s time to start looking for an alternative now. It is much less risky to test a new solution while the old rules are still in place than to "cold start" in July.

Re-forecast Your Cash Flow: Meet with your accountant to work out how the new weekly or fortnightly super payments will affect your cash flow. You may need to rework your drawings or credit facilities.

Consider New Hires: There is a small exception for new employees—the normal rule is that an employer has 20 business days from the first payday to make the first contribution into a new starter’s fund. Take the time to understand these “onboarding” provisions to avoid accidental penalties.

The Silver Lining: Tax Deductibility

In a rare piece of good news for employers, the new legislation clarifies that late SG contributions and the SGC (including the interest and admin uplift) will generally be tax-deductible. Under the old law, late super payments were a "black hole" of non-deductibility. This change recognizes that in a high-frequency payment environment, even the best-run businesses might occasionally trip up.

Payday Super marks a shift toward real-time payroll compliance in Australia’s digital economy.

Conclusion

The shift to Payday Super on July 1, 2026, marks the end of an era. It is a change from "batch processing" to "real-time compliance."

While the administrative burden is increasing, the move aligns Australia’s retirement system with the modern digital economy. For business owners, the message is clear: Preparation is the best defense. By auditing your payroll systems and managing your cash flow management today, you can ensure that when July 2026 comes around, your business will be ready to hit the ground running.